X

CLient Portal

Is expatriation on the rise? According to a 2020 report from the US Department of the Treasury, the answer is a resounding yes. In just the first three quarters of that year, the report revealed that a record number of US citizens had expatriated from the US.

The data is clear: more American citizens are wishing to renounce their US citizenship than ever before. We can only speculate on the reasons for this increase, but a major driver may be taxes. While many people choose to live and work abroad without giving up their US citizenship, others are frustrated by the US taxation system and how high US taxes affect their ability to live and thrive elsewhere.

In this article, we use the term expatriation in the context of the US tax system, which means an individual has chosen to renounce their citizenship or relinquish their green card for federal tax purposes. It should be noted that unless US citizens have dual citizenship somewhere else, expatriation is not an option for them.

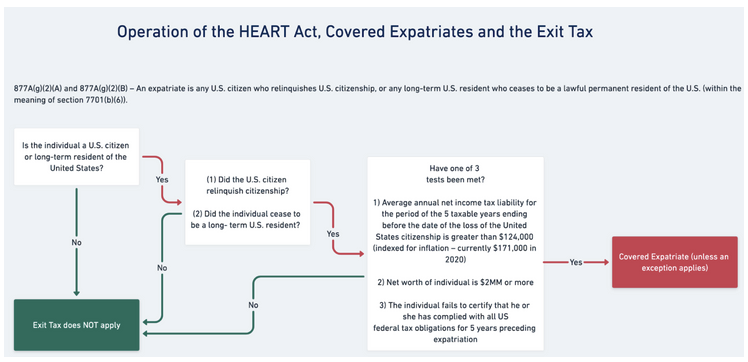

But if an individual does choose to expatriate, it isn’t as easy as simply making a formal renunciation of nationality. Citizens and resident aliens who are considered “covered expatriates” (see below) must also be prepared to pay an exit tax to the US as a result of provisions in the HEART Act.

The Heroes Earnings Assistance and Relief Tax Act was signed into law by President Bush in 2008. Although its main purpose was to provide tax and pension benefits to US military service members, it has significant consequences for US expatriates and resident aliens who choose to leave the US and meet at least one of the qualifications that make them a covered expatriate.

If deemed a covered expatriate, the HEART Act stipulates that the individual must pay an exit tax to the United States government when they decide to relinquish their US citizenship or resident alien status. The HEART Act affects both the income and estate and gift tax systems, so covered expatriates must be prepared to understand how they will be affected on both accounts.

Because the exit tax can be hefty, US tax residents must carefully consider the pros and cons before deciding whether or not to exit the US financial system. If they do decide to exit, they may need to make use of special planning strategies to optimize their financial situation.

Typically, the HEART Act affects US citizens – either by birth or by parentage – who renounce their citizenship. The HEART Act also affects long-term resident aliens who have been lawful permanent residents for at least eight of the last 15 taxable years ending with the year in which they terminate their residence.

However, the HEART Act doesn’t affect all US citizens and resident aliens, but those who are considered “covered expatriates.” An individual is considered a covered expatriate if one or more of the following circumstances apply to them:

Unlike prior legislation, the HEART Act no longer requires covered expatriates to give notice of their expatriation date or termination of residency. Now, a US citizen or resident alien is subject to the exit tax at the earliest of four possible dates:

Once you've determined if you will be considered expatriate, it's time to start looking at strategies for your most optimal outcomes when you plan to exit the US. It may be in your best interest to hire a fiduciary financial advisor who is experienced in advising expats.

There are a few exceptions to individuals who are subject to the exit tax outlined in the HEART Act. Individuals who relinquish their U.S. citizenship before age 18½ are exempted from the exit tax if they were a resident of the U.S. for no more than 10 taxable years before such relinquishment.

Additionally, individuals born with citizenship in both the United States and another country may not be subject to the exit tax. If the individual continues to be a citizen and resident of their other country and they have not been a resident of the U.S. for more than 10 of the 15 taxable years ending with the taxable year of expatriation, they are exempted from the exit tax.

Under the HEART Act, covered expatriates must pay a tax known as the mark-to-market exit income tax. This means that they must pay a tax on all net unrealized gain on all property as if they had sold for its fair market value on the day they are expatriating. Net gains on this hypothetical “sale” are recognized if they exceed a certain threshold that is adjusted for inflation ($737,000 in 2020, $744,000 in 2021).

US citizens or residents must also pay estate or gift taxes on any property acquired from a covered expatriate. Likewise, US citizens or resident aliens who make gifts to non-US citizens (including non-US citizen spouses) must also pay a gift tax if the gift exceeds the lifetime gift exclusion limit.

Although the mark-to-market exit tax can be cumbersome for expatriating individuals, it’s not the only thing they and their financial advisors must consider. There is also the US inheritance tax, which can apply to expatriates even long after their expatriation date, and indeed up until their death when their wealth passes to US inheritors.

Unfortunately, the US inheritance tax as it applies to expatriates does not just apply to wealth held at the time of expatriation. The inheritance tax may apply to all wealth an individual has accrued over their lifetime even after they’ve expatriated. US expatriates who plan to leave money to US citizens to resident aliens must consider US tax consequences in their estate planning even if they no longer have individual ties to the US.

At Areté Wealth Strategists Australia, we support expatriates and resident aliens with all their financial planning needs. We know that making the decision to relinquish your citizenship or green card can be daunting, to say the least, and you have many things to consider in terms of your tax planning decisions.

We want to help. Among other things, we provide ongoing education and support to our clients regarding complex laws and regulations like the HEART Act. To learn more about how we help our clients make the right decisions for their financial situation, give us a call at 888.544.3250 or find a time on our calendar that works for you. We look forward to hearing from you!

.png)

Access our comprehensive, unbiased financial guides here.

.webp)

.webp)

.webp)

.webp)

.png)

.png)

.png)

.png)

%20(1).webp)

.webp)

.webp)