X

CLient Portal

In this article, we provide an overview of the inheritance process for both U.S. tax residents and non-U.S. tax residents who live in Australia and inherit U.S. assets.

U.S. gift or estate tax are collectively known as ‘transfer taxes’ as they’re assessable when property transfers from one person to another.

A U.S. tax resident (i.e. a U.S. citizen or U.S. permanent resident) living in Australia is subject to transfer taxes on their worldwide estate. These individuals however, are eligible for a lifetime unified gift and estate tax credit of $12.92 million USD (in 2023, indexed for inflation annually). That is to say, at current levels, a U.S. tax resident living in Australia may gift or pass on an estate worth up to $12.92M before any estate or gift tax would be due. This amount is currently scheduled to decrease to about $6.2 million USD in 2025 as a result of the Tax Cuts and Jobs Act in 2018.

Australia doesn’t have an estate tax. Despite not having an estate tax, Australia still taxes assets from the sale of a deceased estate as there is no step-up in basis on most investment assets (although there are some exceptions for tax dependents inheriting a superannuation account or a primary residence).

In addition, income and gift taxation in Australia is handled solely by the ATO. In the U.S., in addition to the federal estate tax, each state may also have its own estate and/or inheritance tax.

In 1953, the U.S. and Australia signed an Estate and Gift Tax treaty. This treaty serves two purposes:

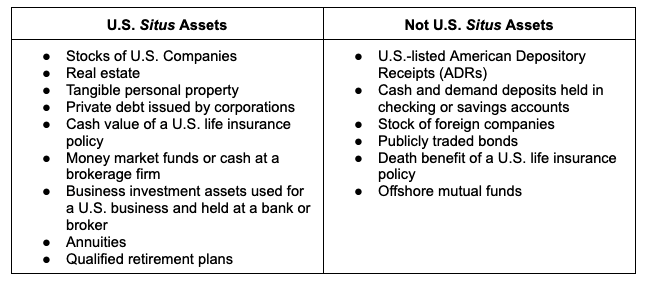

The situs of an asset is the legal location of the asset for purposes of taxation, ownership, and other legal matters.

Why is this important? The situs will determine the tax authority that oversees the asset and how it is distributed.

The situs of real estate is easily determined—the physical location of the property is the situs.

Situs is less easily determined with other types of assets, such as stocks, and life insurance.

Here is a quick summary of different asset types, and their situs:

Different U.S. states have different rules regarding estate and inheritance taxes. Most states do not impose either tax. However, some states impose an estate tax, while others have an inheritance tax. Only one state—the state of Maryland—imposes both.

The type of tax tells us who is responsible for any taxes upon the passing of an estate:

Estate tax: The estate tax is a tax levied on the estate of a deceased person. Presently Connecticut, Hawaii, Illinois, Maine, Maryland, Massachusetts, Minnesota, New York, Oregon, Rhode Island, Vermont, Washington and Washington D.C. have a State estate tax.

Inheritance tax: The inheritance tax is a tax levied on the beneficiary of an estate. Thus, the inheritance tax is generally paid by the recipient of the assets, not the estate. Presently Iowa, Kentucky, Maryland, Nebraska, New Jersey and Pennsylvania have a State inheritance tax.

If you inherit U.S. property located in a state that levies an estate tax, the estate (giftor) is responsible for any taxes owed. If you inherit U.S. property located in a state that levies an inheritance tax, then you will be responsible for any taxes due.

As a rule, we can say that all U.S. retirement accounts that provide the account holder with a tax deduction on contribution (e.g. 401K, 403b, Traditional IRA, SEP, SIMPLE IRA) will provide tax free accumulation but, importantly, ordinary taxable income upon qualified distribution.

Prior to the SECURE act of 2019, non-spouse beneficiaries who inherited assets in employer retirement plans and IRAs could spread out the Required Minimum Distributions—and thus the tax obligations of distributing the funds—over their lifetimes (aka as a ‘Stretch IRA’).

The SECURE Act changed this so that if a non-spouse beneficiary is 10 years younger than the original account owner, they must liquidate the inherited account within 10 years. In most situations, this will come with a higher tax burden for the beneficiary.

An Australian beneficiary of a U.S. retirement account, post-SECURE act will therefore need to distribute the account over a 10 year period.

The Australian tax treatment of tax-deductible and post-tax (e.g. ROTH) U.S. retirement accounts don’t differ. Both types of accounts are treated as foreign trusts with any growth above the employer and employee contributions assessed as taxable Australian income.

Does this mean the beneficiary of a U.S. retirement account will owe double tax? Likely not, as Australia provides a foreign tax credit on the U.S. tax paid, which, as already stated, is treated entirely as ordinary income, and thus likely has a higher tax burden.

For the purposes of capital gain assets (e.g. investment accounts or investment property), Australia will look to the original cost basis of a capital gain asset whereas the U.S. provides a step up in basis to the fair market value of the asset at the owner’s date of death.

The tax treatment is the same for both U.S. tax residents and non-U.S. tax residents when inherited U.S. real estate. As already mentioned, real-estate, an asset that is situs-ed where physically located, may be taxed at a State and Federal level depending on where exactly it’s located in the U.S.

Assuming a beneficiary is a primary Australian tax resident, there may be additional Australian taxes owing if the Australian assessment is greater than that of the U.S. assessment.

The death benefits from a U.S. life insurance policy are tax free on the U.S. side and likely tax-free in Australia also.

Here we present the case study for James and Patricia Albertshire. James and Patricia are a couple who live in Australia.

While they are both Australian residents, James (59) is a U.S./Australian dual citizen, and Patricia (61) is an Australian citizen.

They are both named as each other's primary beneficiaries with their daughters as contingent beneficiaries.

Of their total assets, some exist only in James's name, some are only in Patricia's name, and some are joint assets.

If James died today, what does the distribution of his assets to Patricia look like?

As James is a U.S. tax resident, his worldwide estate will be subject to U.S. estate tax. Thus, we need to calculate his worldwide estate.

Assets held in joint title are counted 100% in James's estate. Thus, the total amount of James’s estate will be assets held jointly and assets solely in James's name. The only asset not held in Joint title or in James’s name is Patricia’s superannuation account.

The estate consists of the following assets to be inherited:

As James died before 2025, didn’t make any taxable gifts during his lifetime and because his estate was less than $12.92M (in 2023), there will be no U.S. federal estate tax owed by the estate. If James had passed away after 2025, as law presently stands (even post SECURE Act 2.0) any amount above $6.2 million will be taxed at 40%.

We still need to go through the final step to determine how/if his assets should be taxed as they’re distributed to Patricia.

Cash account

Here, there will be no tax due to the U.S. or Australia.

Investment Portfolio of U.S. Stocks/ETFs/Mutual Funds

No tax due on transfer. The portfolio receives a step-up in basis by the U.S. but not by Australia. At the time of sale, the capital gains tax on the Australian side would likely be much greater than the U.S. assessment given the lack of step-up.

Superannuation

Patricia is an Australian tax-dependent beneficiary of James, so the superannuation will pass without any tax implications.

Traditional IRA

Here, things get more complex. In the eyes of the U.S., Patricia is a non-resident alien. She would open an Inherited IRA account, and roll over the funds to that account. Patricia will distribute the account to Australia over her life expectancy as she is a spousal beneficiary.

A foreign tax credit will be generated that can be applied to offset the ATO tax assessment.

Unfortunately, the ATO does not step up this account. An ATO private ruling states that the growth in the account that is not the corpus of the account is taxable. Thus, the original basis that James had in the traditional IRA will pass to Patricia.

Real Estate

If the real estate is left unsold, Patricia only needs to file annual Colorado and U.S. income tax returns. If it is sold, U.S. federal and state taxes are owed, and possibly Australian taxes if the assessment is greater than the U.S. assessment. Fortunately, U.S. state taxes are eligible for an Australian tax credit.

If you are an Australian resident and inherit U.S. assets, you may face different tax implications depending on the type of asset inherited, situs, and whether you are considered a U.S. tax resident or non-U.S. tax resident. Given the complexities of cross-border inheritances, this makes personalized financial planning essential for Australians who inherit U.S. property.

For most people in this situation, the best course of action is to seek guidance from a financial professional who is experienced in handling cross-border inheritances.

At Areté Wealth Strategists, we have years of experience helping Australians with U.S. inheritances navigate the tricky waters of cross-border financial planning.

Visit our website to learn more about how we can help you. When you’re ready to reach out, get started with your free consultation.

.jpeg)

Access our comprehensive, unbiased financial guides here.

.webp)

.webp)

.webp)

.webp)

.png)

.png)

.png)

.png)

%20(1).webp)

.webp)

.webp)